Here’s the thing. Finance can be a dry and boring subject, right? BUT if you could learn all about managing money while having fun at the same time, it sounds like a dream. Well, it’s true that we can learn financial concepts through online games. Not only do they make learning about finance entertaining, but […]

5-Day Master Your Money Challenge is here!

Quick story time. I started this year sort of haphazardly launching my ko-fi shop. Honestly, I just wanted to start. No concrete plan on what to do with it yet. I just wanted to explore a potential source of additional income stream (either through my own shop oooorrr as a new skill to offer to […]

How to Save for Your Dream House: 5 Ways to Keep Your Money Saving Goals

A house is perhaps one of the largest and most important purchases we make in our lives. Like many young professionals out there, you may be thinking about how you can save more to finally buy a house you can call your own. And while setting the intention is a great first step, the most […]

5 Things to Consider Before Investing

“𝑃𝑎𝑎𝑛𝑜 𝑘𝑜 𝑚𝑎𝑝𝑎𝑝𝑎𝑙𝑎𝑔𝑜 𝑎𝑛𝑔 𝑝𝑒𝑟𝑎 𝑘𝑜? 𝑆𝑎𝑎𝑛 𝑏𝑎 𝑚𝑎𝑔𝑎𝑛𝑑𝑎 𝑚𝑎𝑔-𝑖𝑛𝑣𝑒𝑠𝑡?” I often see these questions posted on many finance-related communities in Facebook. Of course, it makes a lot of sense. Who wouldn’t want to grow their money? Ika nga, 𝑚𝑎𝑘𝑒 𝑚𝑜𝑛𝑒𝑦 𝑤𝑜𝑟𝑘 𝑓𝑜𝑟 𝑦𝑜𝑢 𝑖𝑛𝑠𝑡𝑒𝑎𝑑 𝑜𝑓 𝑦𝑜𝑢 𝑤𝑜𝑟𝑘𝑖𝑛𝑔 𝑓𝑜𝑟 𝑖𝑡. Nakaka-excite isiping hindi na tayo […]

How much insurance do you need?

One of the first steps in buying life insurance is determining how much coverage you will need. Your life insurance purchase should be a part of a larger financial plan, taking into consideration any strengths or gaps between your current situation and your financial goals. Why do you need insurance? Life is unpredictable. Whether we […]

How to Price Your Freelance Services: Know your Minimum Hourly Rate

Updated: April 27, 2021 One year into the pandemic, many have transitioned into online freelancing. I’ve seen many posts on several Facebook groups for freelancers asking if it’s okay to charge X dollars per hour for a full-time or part-time position. In efforts to help newbie freelancers out there, I thought I should update […]

Influencer Marketing for Hotel and Restaurant Businesses

We were recently invited to speak before some members of the local business group of entrepreneurs in the hospitality industry, IHARRA (Iligan Hotel and Restaurants and Resorts Association). After their general assembly, three members of Iligan Bloggers Society, Inc. had a short presentation on different social media topics. I wanted to discuss about influencer marketing, a […]

Planner Nerd | Free Printable Finance Tracker

November 2019 Update: I created a minimalist version of this planner and added a few pages. Get the new financial planner here. I am a self-confessed notebook geek, to-do list junkie, or maybe borderline planner nerd. It’s how I push myself to be productive and accountable. It just gives a different sense of accomplishment every […]

Financial Empowerment with Lenddo

On October of 2010, during my first-ever stint as a speaker (naks!), I spoke about the need of businesses to be visible in social media. Social Media is a wide landscape. It includes blogs, microblogs, social networking sites, games, etc., etc., etc. Let’s face it. Social media now takes up a huge chunk of our […]

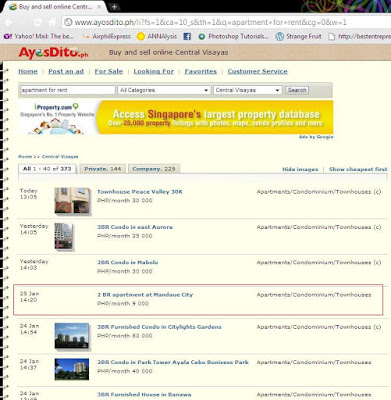

Investments and the Internet

Recently, in our Financial Management class, we’ve been discussing about investments – how to invest, where to invest, and how to manage investments. We also tackled about the importance of diversification of businesses, which is one great way of reducing the risk of losses. Diversification is simply investing in two or more industries which are […]